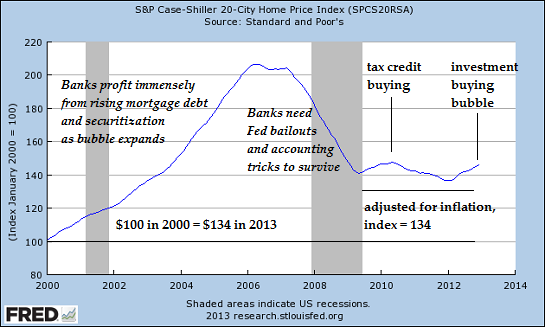

Many people claim the Federal government and Federal Reserve are trying to inflate a new housing bubble to trigger a new "wealth effect," i.e. people seeing their home equity rising once again will feel encouraged to borrow and blow money like they did in 2001-2008. But if we look at current income (down) and debt levels (still high), there is little hope for a renewed wealth effect from housing. That leaves us with this conclusion: The Federal government and Federal Reserve are trying to inflate another housing bubble to save the "too big to fail" banks from a richly deserved day of reckoning.

The housing bubble enabled big banks to skim tens of billions of dollars in profits from originating mortgages to marginal buyers and securitizing mortgages into MBS. This is the heart of what I call the Neocolonial Model of Financialization: rather than make risky sovereign-debt loans to international borrowers, the big U.S. banks came home and exploited the low-risk domestic housing/mortgage market.

The Fed and Federal government immediately stepped in to save their treasured partner, the parasitic banking sector, from righteously earned destruction. The bailouts, guarantees and backstops totaled about $23 trillion, roughly 150% of the entire American Gross Domestic Product (GDP), and roughly twice the 2008 value of all U.S. residential mortgages (almost $12 trillion).

No comments:

Post a Comment