Despite President Obama’s emphatic assurances in the State of the Union Address that “our economy is growing and creating jobs at the fastest pace since 1999,” there have recently been some uncomfortable squiggles, so to speak.

The collapse in the prices of oil, natural gas, and natural-gas liquids has started to make its imprint on the largest hydrocarbon producer in the world, namely the US of A. Oilfield layoffs and project cancellations are raining down on the oil patch on a daily basis. Suppliers are hit too. Many energy stocks are in the process of evisceration. Energy junk bonds are in a rout.

But consumers love it – those who aren’t losing their jobs over it – because they spend less on fuel. Consumers are voters. So politicians love it because voters love it. Hence, it’s good for the economy. I get that.

These sorts of squiggles have been worming their way into national numbers. For example, Markit’s Services PMI for December dropped to 53.3, down for the sixth month in a row, after having peaked in June. This was “not just a one-month wobble,” the report said, as the economy “lost significant growth momentum at the close of the year.” But it remained above 50, the dividing line between expansion and contraction. It’s still an expansion, and “growth is merely slowing from an unusually powerful rate rather than stalling.”

The Manufacturing PMI for December fell to 53.9, down for the fourth month in a row, from the peak in August. Production volumes rose at the weakest pace in 11 months. Same song: Still a “solid expansion,” but at a slower pace. Turns out, “uncertainty towards the global economic outlook had contributed to slower production growth and softer new business gains during recent months.”

The ISM Purchasing Managers Index fell sharply in December, down for the second months in a row, but still in expansion mode. Other indicators piled on as well: on a national basis, the economy seems to be humming along and expanding, but at a slowing pace.

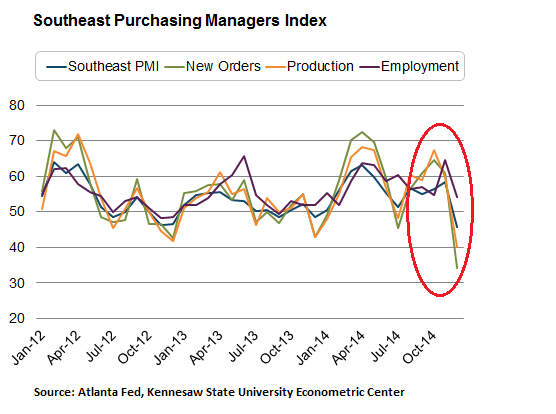

Then comes along the Southeast manufacturing PMI, by the Kennesaw State University Econometric Center, that the Atlanta Fed uses. It covers Alabama, Georgia, Florida, Louisiana, Mississippi, and Tennessee. And in December, it plunged 12.7 points to 45.6.

Below 50. Not “slowing growth,” but an outright contraction. Decembers can be crummy in the Southeast, and these kinds of indices can be volatile, but this was the worst month since December of crisis-year 2009.

And it was crummy across all sub-indices:

- New orders plunged a breath-taking 27 points to 34, blowing with some panache through the magic 50-point mark. Orders essentially evaporated; a harbinger for what might happen next.

- Production dove 19.8 points to 40, a steep contraction.

- Employment dropped 10.6 points to 54, remaining in expansionary mode.

- Supply deliveries fell 7.3 points to 50, the flat line.

- Finished inventory edged up 1.2 points, also to 50.

- Commodity prices dropped 10.4 points to 42, in contraction.

No comments:

Post a Comment